Architecture of Costs

Prepaid cards are funded instruments that allow spending up to the loaded balance. Their cost structure is layered: an issuer may impose card issuance or shipping fees; reload costs when adding funds; conversion spreads or explicit FX fees when spending across currencies; ATM withdrawal charges; and dormancy or service fees for unused balances. The network—Visa or Mastercard—provides settlement rates and infrastructure, but the issuer frequently sets the consumer-facing rate or margin. Visa states that it “provides daily FX rates for the 180+ global currencies that are used within VisaNet to authorize and settle transactions.”

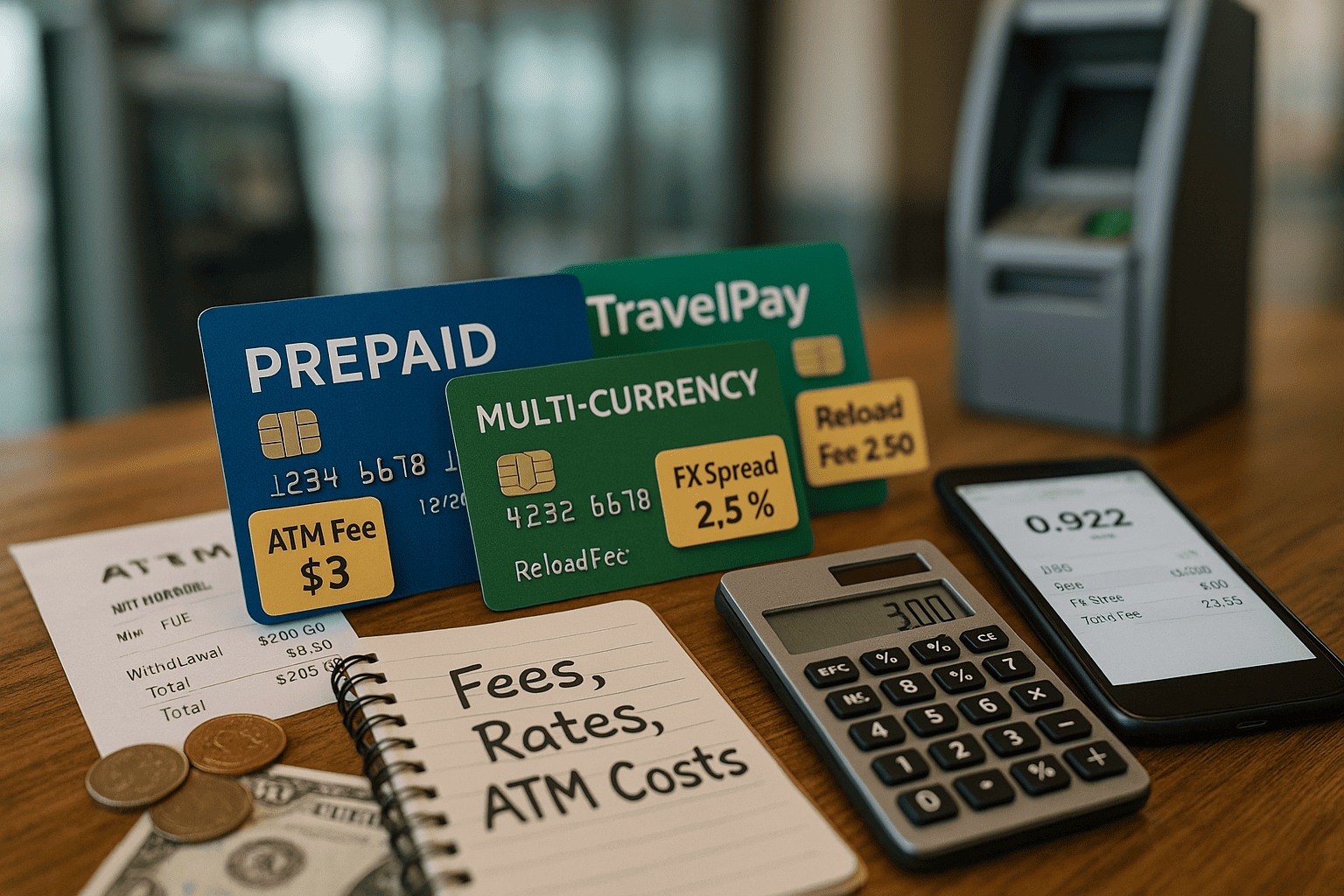

A commercial example that exposes typical layering appears in provider published schedules. One cross-border payout and card provider lists ATM withdrawals as: “Cash withdrawals (ATM, teller, merchant) in the same currency as your card 3.15 USD / 2.50 EUR / 1.95 GBP + UP TO 1.8% ; Cash withdrawals (ATM, teller, merchant) involving currency conversion 3.15 USD / 2.50 EUR / 1.95 GBP + UP TO 3.5%.” That format—flat amount plus percentage—recurs across issuers and is a straightforward way to model marginal ATM cost.

Exchange logic is the single most consequential determinant of real cost. Some issuers convert at the mid-market rate and state this openly. A prominent provider asserts: “We only use the mid-market rate — the one you can check on Google.” That claim eliminates hidden FX markup if fully implemented. Other providers route conversion through network rates and then add an issuer margin; that produces an effective spread that consumers must quantify before loading material sums.

Where Prepaid Card ATM Fees Come From

Two independent actors can create an ATM cost at point of withdrawal:

- The card issuer may charge a withdrawal fee (flat or percentage), often with a monthly free allowance beyond which a fee is applied.

- The ATM owner (bank or independent operator) may impose a terminal surcharge that appears on the screen before acceptance.

Operationally, the issuer may advertise “no issuer fee” while the terminal owner’s surcharge still applies. The practical outcome is that consumers frequently face a combined cost that is higher than the issuer’s advertised policy alone. Revolut’s published guidance makes the user-facing rule explicit: plans provide a free-withdrawal allowance; once that allowance is exceeded, “A 2% or 1 € fair usage fee applies thereafter.” The platform also notes that ATM operator fees are separate.

Modeling total cash cost therefore demands checking both the issuer fee schedule and the ATM owner’s displayed charge at the time of withdrawal.

How Exchange Rates Are Applied

Three execution models dominate observed practice:

- Mid-market execution. The issuer passes the interbank rate to the customer and either takes no markup or charges an explicit, disclosed fee for conversion volume. Wise frames the mid-market rate as “the ‘realest’ — and fairest — rate out there,” and reiterates the promise to use that rate for conversions.

- Network conversion with issuer margin. The card networks provide a settlement rate; the issuer layers a percentage margin and publishes a single blended rate to the consumer.

- Flat markup. The issuer adds an explicit spread on top of the network or market rate and presents the final rate as the consumer-facing price.

Small percentage differences compound over routine spending. For instance, a 1.5% effective FX spread on repeated transactions will exceed most nominal flat ATM fees after modest usage. That arithmetic is why published comparisons of the best international prepaid debit cards repeatedly focus on the exchange methodology as the top comparator metric.

Examples From Major Providers

Public pages and fee tables supply repeatable examples for testing.

- Wise positions itself on mid-market conversion and transparent per-conversion pricing. Wise’s public materials explain mid-market sourcing and stress that users see the rate before converting. https://wise.com

- Revolut publishes plan-based free-withdrawal thresholds and the fair-usage fallback: “A 2% or 1 € fair usage fee applies thereafter.” Users should note that this fee sits atop any ATM owner surcharge. https://www.revolut.com

- Payoneer’s pricing page itemises cash withdrawals with a flat component and a percentage: the page lists “Cash withdrawals (ATM, teller, merchant) in the same currency as your card 3.15 USD / 2.50 EUR / 1.95 GBP + UP TO 1.8% ; Cash withdrawals (ATM, teller, merchant) involving currency conversion 3.15 USD / 2.50 EUR / 1.95 GBP + UP TO 3.5%.” That disclosure is usable as a real-world test case for modelling ATM cost on a reloadable international prepaid card. https://www.payoneer.com

Practical Tests That Reveal Effective Cost

A defensible international prepaid debit cards comparison should include three simple checks the buyer can run before committing funds:

- Small live purchase. Load a modest amount in the issuer’s app, make a point-of-sale transaction in the target currency, and capture the exact converted amount on the receipt. Compare that amount to the mid-market quote at the same timestamp.

- ATM withdrawal test. Withdraw the smallest available amount from a common ATM, note the issuer line item in the card transaction feed, and confirm whether an ATM operator surcharge was presented on the screen. Record the flat and percentage components.

- Reload variance check. Top up by bank transfer and by card; compare time-to-credit and any processing fees. For travel planning, bank transfers often minimise extra charges.

Independent consumer organisations that produce lists of top prepaid travel cards run similar tests and publish methodologies; Which? and Forbes Advisor provide accessible comparison frameworks that can be followed for individual due diligence. https://www.which.co.uk, https://www.forbes.com/advisor/

Behavior That Erodes Value

Three common traps consume value without obvious signals:

- Inactivity charges or account servicing fees when balances sit unused. Some issuers deduct small monthly amounts after a dormancy period; those micro-deductions accumulate.

- Weekend or out-of-market hour markups. Several issuers disclose worse conversion margins when markets are closed. The cumulative effect is higher cost for last-minute or weekend conversions.

- Multiple micro-charges across low-value transactions. Small per-transaction percentages hit low-spend patterns particularly hard.

Regulators monitor disclosure practices because these multi-layered fees produce consumer detriment when not plainly stated. The European Banking Authority lists promoting “transparency, simplicity and fairness in the market for consumer financial products or services across the internal market” as an information objective for supervisory activity. https://www.eba.europa.eu

How to Choose

Prioritise issuers that clearly state whether they use mid-market rates or an issuer margin. That declaration is the single best predictor of long-run FX cost. Test prepaid card ATM fees with a live withdrawal before travel and include terminal surcharge checks in the test. Use small live transactions to validate advertised behaviour and reconcile receipts to public mid-market quotations.

Final Considerations

Prepaid debit cards for travel and multi-currency prepaid cards can reduce FX opacity when issuers pass near-mid-market rates and keep reload and withdrawal fees low. Nonetheless, effective cost depends on the composite of issuer pricing, network settlement, and ATM operator surcharges. The prudent buyer treats marketing claims as hypotheses and converts them into verified economics through three short experiments: a purchase, an ATM withdrawal, and a reload test. Those empirical checks, combined with reading the issuer’s published fee table and noting dormancy terms, convert opaque fee schedules into actionable cost expectations and reduce the risk that the card becomes an unexpected expense rather than a convenience.

Selected sources and further reading: Wise — pricing and mid-market explanation, Revolut — ATM rules and fair usage fee, Payoneer — published ATM and conversion fee table, Visa — FX rate provision for VisaNet, Which? — independent comparison frameworks, Forbes Advisor — independent comparison frameworks.